John Piercey's Vision 2025 financial summary

As I mentioned in last week's Urban Tulsa Weekly, a few weeks ago I began my search for the source of the numbers being cited in defense of the need to raise taxes to build the two low-water dams and the Zink Lake modifications promised in Proposition No. 4 of the Vision 2025 sales tax.

The debate over this issue has two prongs:

(1) Did Tulsa County officials promise to build the dams during the Vision 2025 campaign? And did they promise that they'd have the money to build them even if Federal matching dollars weren't available? Despite word-parsing efforts by Commissioner Randi Miller and others, the clear answer to that question is yes, as I've demonstrated from the official ballot resolution, the official project map used during the campaign, and quotes from Commissioner Bob Dick and others during the campaign, and even after the campaign, when Federal funding was once again in doubt.

(2) Is there enough money in projected Vision 2025 revenues to cover the cost of the new dams and the Zink Lake modifications? County officials, citing numbers developed by John Piercey, the county's bond adviser, say that the answer is no. Based on revenue projections, remaining projects to be funded, and debt service, there isn't enough money, they say to fund the low water dams beyond the specific amounts listed in the resolution, much less fund any other project on this October's ballot.

That second point set me off on a search to find out for myself. I combed through the five big binders of monthly Vision 2025 reports in the fourth floor Government Documents department of the Central Library. (The most recent three binders are in the work room, so you need to ask at the reference desk if you want to see them.)

Having looked at the sales tax summaries and project summaries in the monthly reports, I had a simple mental model of how it all fit together. You had two pots of money: A pot of sales tax revenue and a pot of bond proceeds.

Sales tax receipts come into the sales tax revenue pot, and from that pot comes bond repayment (debt service: principal and interest) and cash expenditures (e.g., money to pay down the Oklahoma Aquarium debt, fees to PMg and attorneys).

The bond proceeds pot is fed by proceeds from revenue bond sales, and that money is spent on expenditures for most of the projects.

So what I wanted to know was this:

(1) How much money was in each pot as of, say, the end of the fiscal year on June 30, 2007?

(2) How much money was likely to be added to the sales tax pot between now and the last sales tax check in February 2017? (There's about a month and a half delay between collection and the resulting check from the Oklahoma Tax Commission back to the cities and counties.)

(3) Of the money in the sales tax pot, how much is committed to debt service, and what is the repayment schedule?

(4) Of the money in the sales tax pot, how much is budgeted but yet to be spent for projects and for overall program expenses, and what is the schedule for spending that money, and for which projects?

(5) Of the money in the bond pot, how much is budgeted but yet to be spent for projects and program expenses, and what is the schedule for spending that money, and for which projects?

I figured that, with all the talk about how we wouldn't have enough money to build the promised dams, that somebody must have all this worked out, at least on a year by year basis. If you had the answers to those five questions, you could make decisions about borrowing against future revenues or the likelihood of additional money that could be spent on a pay-as-you-go basis or possibly even reprioritizing the sequence in which the remaining projects (including the dam and Zink Lake projects) would be funded.

I wrote about my quest a few weeks ago:

I asked Kirby Crowe by phone if he had a copy of this plan. I'm not sure if I made my meaning clear, but I came away from the conversation with the impression that he did not have a copy of Piercey's financial plan.

I called Jim Smith, the County's fiscal officer, and asked if he had a copy of the financial plan. I thought he might, since his name is on the monthly memo in the Vision 2025 report listing tax receipts, the monthly wire transfer from the sales tax fund to the trustee, and the interest earnings on the sales tax trust account.

Smith said he didn't have the financial plan, but suggested I call John Piercey. Mr. Smith could tell me what the payment to the trustee would be for the next six months, at which point it would be recalculated, but couldn't tell me anything more about future expenses.

I called Capital West, and they gave me John Piercey's number. I called John, and he was very gracious. He said he'd e-mail it to me that evening or the following morning. He said something about recalculating based on more recent tax receipts. I'd really be happy seeing the most recent version, whatever he's been using as the basis for his statements about Vision 2025 surpluses.

That was a week ago Monday, the 20th. I gave him a reminder call on the 28th -- got his voicemail and left a message. Haven't heard back yet. I'm sure he's quite busy.

Can anyone suggest somewhere else I could find this information?

That was on August 30. Eight days later, on September 7, I left another message for Mr. Piercey. I also, on a whim, called County Commissioner Fred Perry's office to see if they have a copy of this rumored financial plan. The administrative assistant didn't know, but she took my message, and about an hour later, Commissioner Perry called me. (Part of that conversation found its way into the update to this entry about the Republican Women's Club's exclusion of the opposition from a discussion of the county river tax.)

Perry told me he would ask Piercey to get me the information, and not long after I heard from Piercey. The following Tuesday afternoon, September 11, he dropped the three-page Excel printout, entitled "Vision 2025 Financial Summary" by UTW's offices. (Clicking that link will open a PDF file, about 300 KB.)

Off and on over the following week, I crunched through Piercey's numbers covering the next nine and a half years and tried to fit them together with the numbers in the Vision 2025 reports covering the past three and a half years, trying to meld them together into a consistent set of answers to my questions.

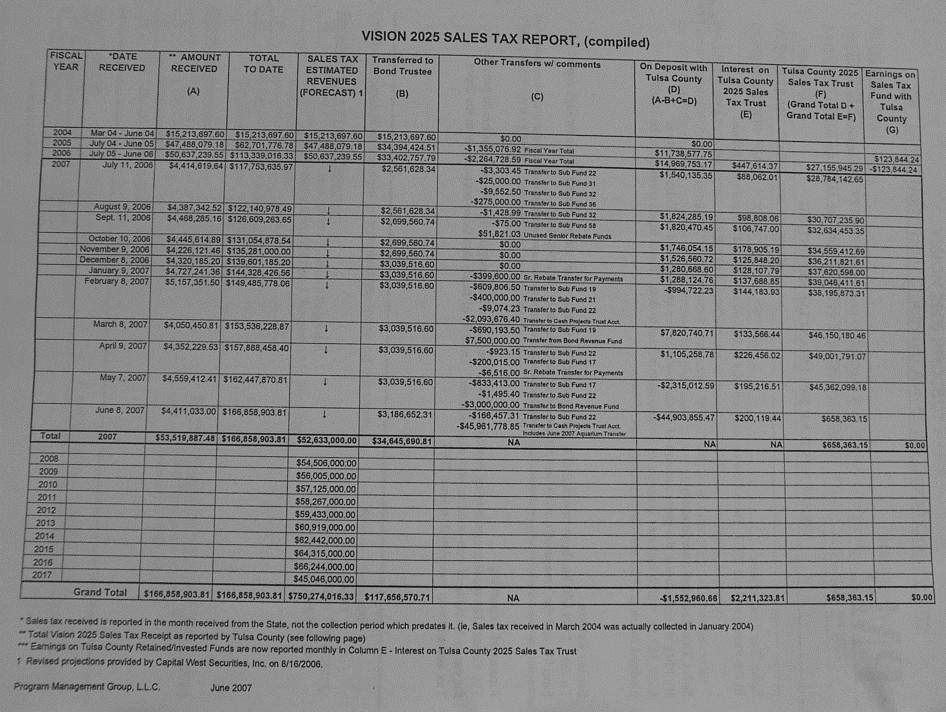

Finally, I sent Piercey an e-mail, attaching a snapshot of the financial spreadsheet from the June 2007 Vision 2025 report:

{kind=link}

John,

Thanks again for providing me with that spreadsheet printout last Tuesday. I'm still looking at it and trying to understand how your numbers line up with the ones I observed in the Vision 2025 monthly reports from PMg.

The most puzzling thing is the gap between previous years debt service numbers and the numbers in your projections. Attached is a photo of the Vision 2025 sales tax report from PMg's June 2007 Vision 2025 report, which includes all receipts and expenditures through the end of FY07. It shows the following amounts transferred to the bond trustee:

FY

Transferred to Bond Trustee

2004

15,213,697.60

2005

34,394,424.51

2006

33,402,757.79

2007

34,645,690.81

I take those numbers to represent what has been paid to debt service to date. So it's puzzling that for FY 2008 that the debt service jumps up to $46,977,024 plus $396,500 for Series 2006 B. Did the debt service payments just jump up at the end of FY 2007, or is something else on that PMg spreadsheet that should be included in debt service to date?

Put another way, what are your numbers for debt service through FY 2007?

(I'm also surprised that the debt service number doesn't tail off in 2017, since there are only eight months of revenue from the tax in FY 2017.)

Another apparent difference between PMg's numbers and yours: PMg shows, after May 2007, $45,362,099.18 in the sales tax trust fund, and in June all of it is transferred to a new cash projects trust account, in addition to about $2 million transferred to this cash projects trust account back in February. You show $39,093,695 as sales tax revenues held by County. I don't understand how those two numbers line up.

Another question has to do with when various expenses and funds might be realized. You show a balance to be funded of $104.5 million and about $69.3 million of cashflow from bond fund reserves ($39.4 million), net earnings on bond funds ($13.7 million), and net earnings on cash flow ($16.2 million). Has anyone mapped out, to the fiscal year, when these expenses and earnings will be realized?

Thanks again for your assistance,

Michael D. Bates

Here is Piercey's reply in full, clarifying the nature of his report and his role with Vision 2025 and Tulsa County:

Capital West Securities, Inc. official involvement with raising additional funds for Vision 2025 ended in the third quarter of 2006 with the completion of the funding of $31 million in parity and subordinate bonds which partially funded the $45.5 million approved by the County for the Arena and Convention Center. The balance of the funds for the projects increased budget will come from cash flow through the end of calendar year 2008.

My current involvement is as an unpaid monitor of the monthly sales tax receipts and the preparation of a semi annual update of the status of the financial condition of the program. The day to day management of the Program is performed by PMG and the funds administration is performed by the Bond Trustee in cooperation with Jim Smith, the County's fiscal officer. The summary that was given to you is the most current semi annual Update that I have done and is not a "financial plan".

The monthly PMG report provided to the elected officials and the Sales Tax Overview committee will differ from my evaluation simply because they are looking primarily at projects implementation and monthly cash flows provided to them by the Trustee and PMG. They will also differ as a result of the time frame that I used and the in and out of money that occurs weekly.

As I pointed out to John Eagleton in a prior correspondence, the debt service payments that are shown in the PMG reports are what the Trustee requires from sales tax receipts on a monthly basis. The difference between the receipts and the payment goes into sales tax trust fund. The sales tax trust fund is being used to fund Vision projects not funded by bond proceeds. It builds up over time as a results of primarily the City of Tulsa budget process which requires all funds to be in place and appropriated before project contracts can be signed.

The Trustee's debt service requirements given to the County differ from the debt service requirements on the bonds are a results of interest earnings on the construction funds held by the Trustee as well as interest earnings on the Bond Fund Reserve account of $39.09 million. Given the amount of proceeds raised early in the program those earnings were substantial in the early years of the program and decline as projects are completed. This will also be the case with the County's sales tax trust fund as the Arena and Convention Center is completed between now and the end of fiscal year 2008.

As for specific answers to your questions:

1. Debt service has risen annually since 2003 as a results of additional bond issues being done as projects became ready for implementation. Debt service has also risen as the amount of investment earnings have declined as moneys are spent.

2. The PMG debt service numbers are net of investment earnings.

3. All the bond issues, except series 2006B, are rated AAA. In order to get a AAA rating, a cash reserve of $39 plus million was funded early in the program and is held by the Trustee. The purpose of the reserve is have sufficient funds on hand to pay debt service in the event that sales tax receipts at any one time or length of time is insufficient to pay the debt service. The Reserve is released in the final year (2017) to pay most of the final year's debt service. This final payment assumes that no short fall has occurred.

4. The Series 2006 B bonds of $10 million are subordinate bonds and are unrated. The reason being that the requirements to issue more bonds on a parity basis could not be met. The $14.5 million in cash flow for the Arena and Convention Center was also the results of not being able to issue more debt without increasing the costs of the debt and the risk that other projects would have to be postponed or possibly eliminated if sales tax receipts declined.

5. The Vision 2025 program included $575 million in specific projects with specific dollar allocations. Of that total 83% were funded by bond proceeds or in the case the Aquarium annual payments were contracted for. The balance of approximately $100 million (excluding the rebate) are being funded by sales taxes and investment earnings remaining after debt service is paid monthly. With the exception of the River Projects which were matching funds, cash flow schedules have been reviewed and PMG schedules those projects as they become ready and/or funds are available.

6. As I have noted in the past, I see no excess funds being available for new projects or increases for approved projects until after 2012-13. I hope that my forecast is too low. The bulk of any future surplus will occur in 2017 as the $39.1 million in bond fund reserve is released.

John Piercey

There's a lot to digest here. I'm putting it all here for anyone who cares to analyze it and comment on it.

One of the discoveries in all this is that there are actually four pots of money. In addition to the bond proceeds and the sales tax receipts, there is a bond repayment trust fund held by the bond trustee (the Bank of Oklahoma). When Jim Smith tried to explain to me how it worked, I compared it to an escrow account for paying taxes and insurance on a mortgaged house, which Smith thought was a good analogy. The bond trustee then repays the bondholders from this trust fund. Every six months, the bond trustee recalculates the payments they need from Tulsa County's sales tax receipts to enable them to pay the bondholders.

Here's my paraphrase of Piercey's explanation of the difference between the payments to the bond trustee (found in the Vision 2025 monthly reports) and his schedule for repayment to the bondholders: The county began paying money into the bond fund as soon as the tax began to be collected, but well before they had to begin to repay the bonds. Those early funds earned interest, which reduced the amount the county had to pay to the bond trustee in order to keep the bond trustee's fund at the required level.

Without the details of the ins and outs of the fund being managed by the bond trustee, there doesn't seem to be any way to correlate the sales tax payments to the bond trustee (in the Vision 2025 monthly reports) with the payments to the bondholders (in Piercey's financial summary). The Vision 2025 monthly reports don't cover the balances and transactions in the bond repayment trust account or in the bond proceeds pot of money. (It just now occurs to me that those two pots may actually be a single pot of money.) There are individual monthly project expenditures in the report, which you can infer are payments from the bond proceeds, but it isn't explicit, and transactions like interest earnings are either not reported or perhaps just not obvious to me. It would be good to have a spreadsheet for the bond proceeds fund that spells things out as clearly as the sales tax spreadsheet does for that fund -- the balance at the beginning of each month, all the income and the outgo, and the balance at the end.

I mentioned that there's a fourth pot of money. The June 2007 Vision 2025 monthly report shows that in February, $2,093,676.40 was transferred to the Cash Projects Trust Account, and in June, $45,961,778.85 -- pretty much the entire sales tax reserve being held in the county's accounts -- was transferred to the Cash Projects Trust Account. A memo included in one of the monthly reports says that this account is also being managed by BOk.

I still don't see a way to answer my five questions from the information available. If I were a County Commissioner or a member of the Vision 2025 Sales Tax Overview Committee, I would insist on putting that information together and updating it on a monthly basis to serve as Tulsa County's financial plan for the Vision 2025 program.

It looks to me that John Piercey, PMg, and BOk each possess different pieces of the puzzle, but that no one has actually put all of it together into a complete picture, a complete plan that would permit exploring different scenarios that would allow the use of Vision 2025 funds to complete the dams that were promised as a part of that package.

There's another aspect of this that needs to be explored, but it's late and I'm tired. I'll just point you in the general direction. On the front page of Piercey's summary are three columns: "Pre-Request," "Arena Increase," "Revised Totals." The difference between the first and third columns tell quite a story.

1 TrackBacks

Listed below are links to blogs that reference this entry: John Piercey's Vision 2025 financial summary.

TrackBack URL for this entry: https://www.batesline.com/cgi-bin/mt/mt-tb.cgi/3059

Just as they did in 2003, Tulsa "leaders" are preying on anxieties about job losses to justify siphoning more of your tax dollars through county government to favored businesses. Two possibilities are being discussed to raise $340 million: Either a cou... Read More

Great reporting Michael. You are a much better reporter than any reporter at the Tulsa World Newspaper.

They should be putting this on all the news channels.

Offhand, and not to jump to conclusions, it appears that rather than three or four entities having different pieces of the complete picture, we have two sets of books, with the other one not yet being revealed.

"It looks to me that John Piercey, PMg, and BOk each possess different pieces of the puzzle, but that no one has actually put all of it together into a complete picture, a complete plan that would permit exploring different scenarios that would allow the use of Vision 2025 funds to complete the dams that were promised as a part of that package."

That sounds like work Mike. Let's just raise taxes instead.

This is at the absolute tops of Michael's investigative / opinion pieces!

Tremendous analysis!

WHERE is the Tulsa World in surfacing this story?

Answer: They spiked it, already. Nothing to see here; just move along.

Stepping back, what we can actually see is one of the power centers that runs our city and, is also a principal promoter of the Kaiser River Tax: Our largest bank.

Not only did they receive half of the Vision 2025 bond Underwriting Business, they also serve as the "Bond Trustee" of the Vision 2025 bonded indebtedness, over the entire life of the bonds. Are they handsomely paid for this service?

Uh, it wasn't competitively bid, right? Or the bond underwriting, either?

Of course, not. It's a COUNTY deal. Openness, transparency, and competitive bidding are eschewed by our County Government.

Uh, and how much did the bank contribute to get Vision 2025 passed?

How much support are they providing to pass the Kaiser River Tax?? Lots??

And, in the meantime, our City Government is in final negotiations to subrogate the Master Lease on the ENTIRE new City Hall with the selfsame entity.

And, if anyone at this bank wanted to, they could literally urinate off their roof onto the heads of our Mayor and City Government offices.

Maybe they already are.....

Get out your umbrella, MeeCiteeWurker.

who knows what the answer is. by the time you get through all the layers, you're exhausted.

the simple truth is, if the dams were promised in myopia 2025, they should not be part of this proposal.

I wouls also ask this. What is the status of the Corps of Engineers study on the placement of those low water dams? Has there been an approval issued by the same Corps of Engineers? If not, the Vote Yessssssssss people are pulling the same scam that was pulled in Myopia 2025. Are we that dense as voters?